Someone move in non-stop. They may move having an alternate employment, on account of an army transfer, or to are now living in a far more beneficial climate.

An universal problem many moving firms face is the must pick an alternate family whenever you are owning another one. It possibly takes a little while for homes to sell, and you may would love to buy a separate https://paydayloansalaska.net/cohoe/ domestic is almost certainly not simpler otherwise you can easily-you might like to be thinking spending!

If you’re questioning ideas on how to get a house while getting a different one, the following are several options to look at.

Play with a connection Mortgage

Link money can be always purchase brand new property whenever man’s most recent property haven’t sold. He or she is short term money which might be designed to bring quick-name resource getting a special domestic. They generally only last six to help you 1 year, and are safeguarded because of the basic house.

Because of the short-term characteristics out of link fund, such money usually have higher interest levels than simply conventional finance. To qualify for a link mortgage, most loan providers require you to possess at the least 20% collateral of your property.

Bridge money are usually accepted from inside the a shorter time than many other domestic investment options, allowing you to obtain fast financing in order to safer a different house during the a trending market. They also enables you to pick a unique home devoid of a backup on the render that requires the first where you can find promote one which just personal on 2nd family.

An essential negative off connection loans to adopt is that certain lenders wouldn’t accept a link financing unless you also thinking about acquiring your new mortgage using them. They also have settlement costs that you will have to blow.

Tap into The Home’s Security

Household guarantee finance also are labeled as 2nd mortgage loans since the collateral you’ve got of your house can be used because the security getting the second loan. Of numerous lenders assists you to obtain around 85% (if not 100%, like America’s Credit Commitment) of your home collateral.

Should you want to see a traditional loan for your the brand new household, a property security mortgage are often used to use the money necessary for a downpayment for the a special house. Should your basic domestic deal, you will be expected to have fun with the main continues to help you pay your house guarantee financing.

Having fun with a house security mortgage so you’re able to buy your 2nd domestic can help you purchase a lot more house than you or even you’ll. Additionally cover the coupons which means you don’t need to put your crisis loans at stake. Because your earliest house is made use of while the guarantee, such money are not too difficult to get.

There are a few crucial downsides to having a house guarantee mortgage to shop for another home to think. Basic, you’ll have to carry out about three loans at the same time. There will be antique fund for the one another the dated and the fresh land. Then there are your house guarantee loan.

You will additionally become putting very first domestic at stake if youre struggling to make payments on the mortgages. Fundamentally, you will also have to invest settlement costs towards the house security mortgage, that can constantly be below 5% of the loan amount.

Rent Your home

If housing industry try scorching, you might have to captivate multiple greatest-money estimates for your house. But when the business cools, it could take a little while for your house to offer. Incase you do get an offer, it can be lower than might prefer.

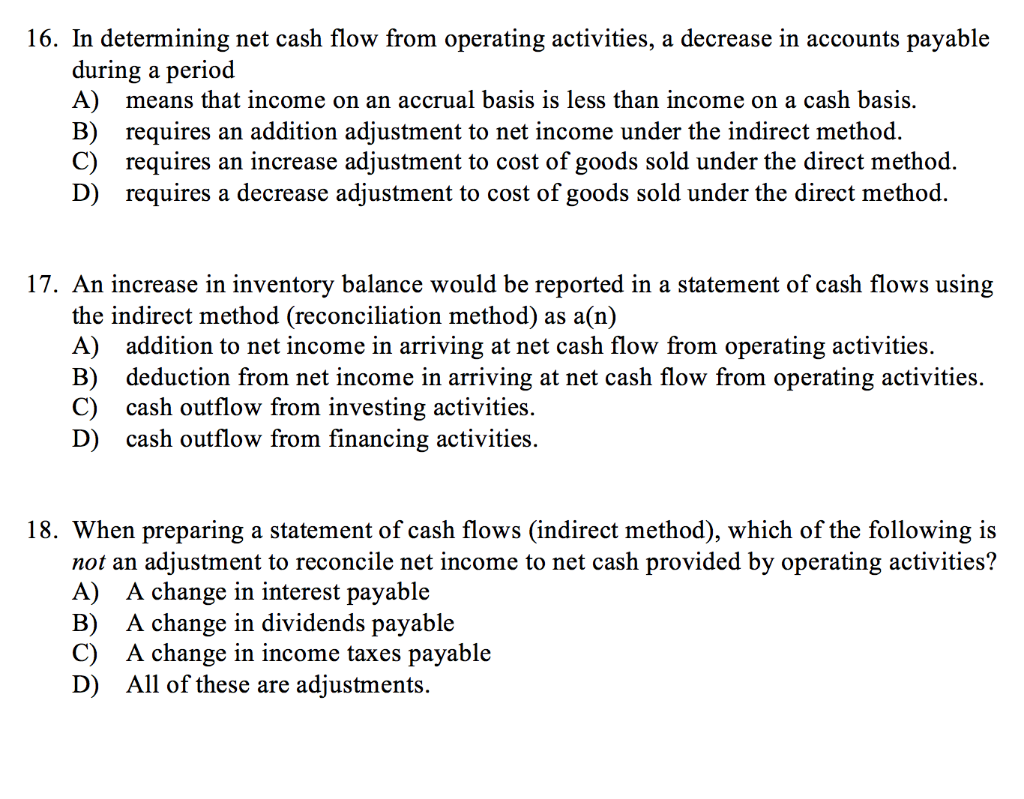

In case the housing industry is actually a beneficial slump if you decide to move, this may add up so you can book your home unlike selling. You need to use the local rental money to pay the mortgage, which can help your build collateral. This allows that wait for a much better housing industry so you’re able to offer.

There are two main methods lease your home. You can either rent it to at least one much time-title occupant, you can also book it to quick-name renters on the websites particularly Airbnb. For each and every solution keeps crucial advantageous assets to envision.

Having a lengthy-name occupant, there will be a steady cash flow, and there’s faster performs inside it. Short-label apartments, yet not, constantly earn more money, although they require way more works. We machine short-name leases remotely. Should you choose, you will have to plan for someone local to cleanse the latest home after every renter.

A solution to think if you’d like to book your property nevertheless should not handle new issues to be a property owner is with property management business. These businesses manage renting your home, writing on tenant items, and other anything. Assets professionals constantly fees 8 to ten% of month-to-month lease.

Va fund was popular with armed forces employees as they enable you to find a property and no downpayment, no PMI requirements, and you will competitive rates of interest. If you find yourself regarding the armed forces, these types of funds could also be used to invest in a second house.

You need a certification out of Qualification (COE) about Virtual assistant so you’re able to qualify for an additional Virtual assistant loan. Including, the fresh new household you are purchasing is employed since your this new no. 1 residence.

For this method to performs, your COE need to imply that you may have sometimes complete or partial entitlement. For folks who bought the first home with a good Va financing, such, you might still provides limited entitlement left. If your mortgage manager demonstrates there’s no entitlement kept, you are going to need to promote your home first before you can fool around with a Virtual assistant loan to order a separate home otherwise have a down payment.

Mortgage brokers having America’s Credit Connection

Periodically you are prepared purchasing but possibly not ready to offer. Help America’s Borrowing from the bank Partnership help you learn to buy property whenever you are managing another one.

- Traditional funds

- Virtual assistant funds

- House guarantee fund

- FHA financing

- Bridge money

Click lower than for additional information on the house funds. Of course, if you have got any questions, one of our representatives is a call aside.